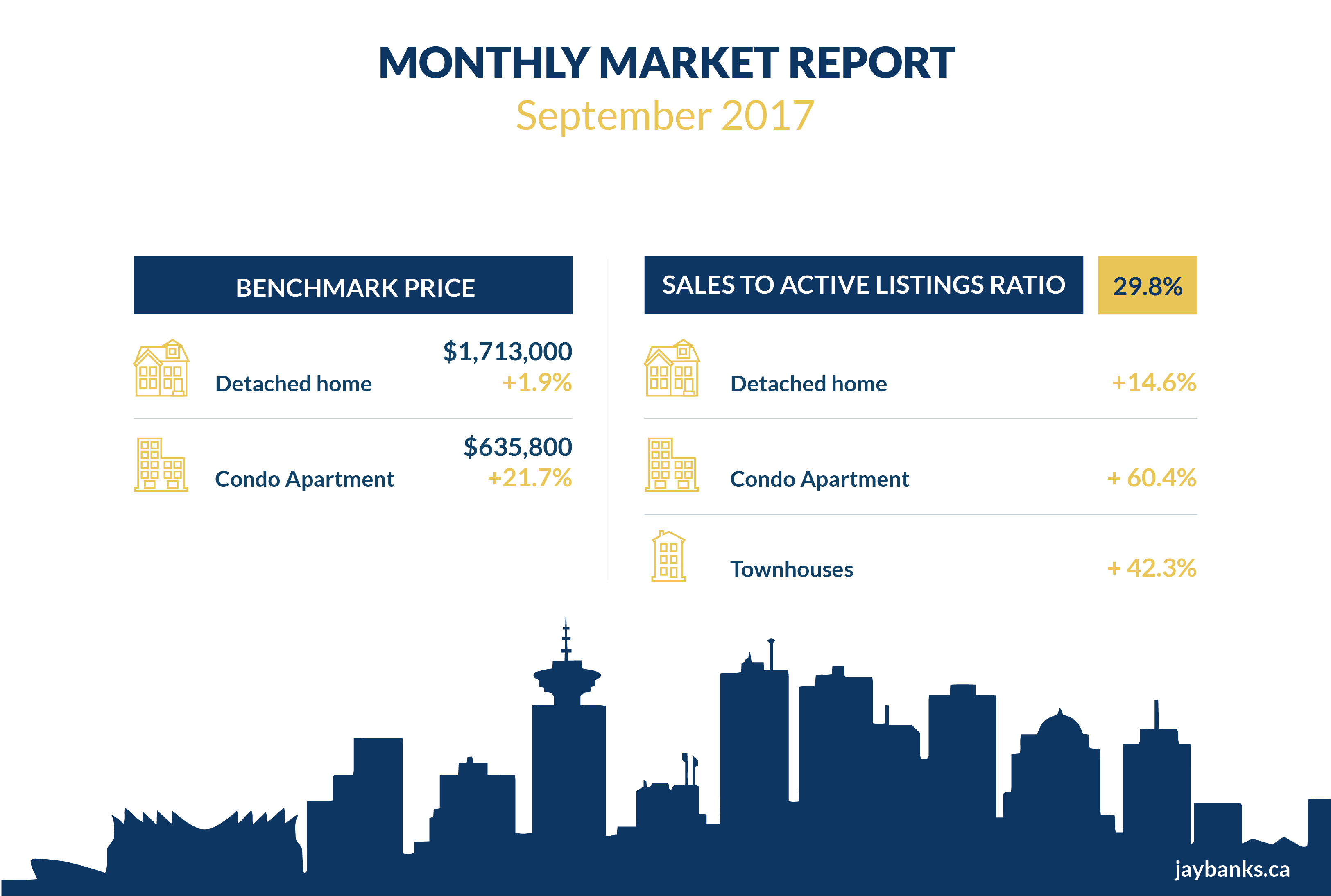

September stats on the housing market are history in the rear view mirror. Changes in the financial world are coming so fast and so furiously that historical information may not apply. Sale prices have risen in every category. Particularly in condo and townhouse segments. Detached homes have gone up a smaller percentage but are still out in the ether as for price.

The sales to active listing ratio for September 2017 is 29.8%.By property type, the ratio is 14.6% for detached homes, 42.3% for townhouses,and 60.4% for condominiums.

In September 2017 the benchmark price for a detached home in North Vancouver was $1,713,000 up 1.9% in one year, up 74.8% in 5 years and up 97.7% in 10 years. In Richmond the benchmark price was $1,695,000 up 1.5% in one year, up 73.3% in 5 years and up 139.4% in 10 years. In Vancouver East the benchmark price was $1,564,900 up 1.8% in one year, up 84.3% in 5 years and up146.2% in 10 years. In Vancouver West the benchmark price was $3,653,500 up 0.8% in one year, up 74.7% in 5 years and up 144.0% in 10 years. In West Vancouver the benchmark price was $3,136,600 down -8.5% in one year, up 67.7% in 5 years and up 105.1% in 10 years. Each year affordability declined for local buyers.

![]() Bentall Tower by Colin Knowles

Bentall Tower by Colin Knowles

There is a sudden realization among the Vision Vancouver city councillors that all the posturing on social and homeless housing took their eye off what was happening with the rezoning projects along transit corridors. Their naivete allowed no restrictions on buildings along the Cambie corridor which should have been zoned for rental housing. The city planner thought that home owners would sell for modest prices so that moderately priced condos would be built there. Instead the Canada Line was built with funds designated for Olympic transit and doubled the prices of the lots. Owners with attractive mid-century and heritage homes sold them for $3 million in 2009 with expensive condos going in all up and down the Line. Now in Phase 3 Mayor Gregor Robertson is bemoaning the lack of rental housing for residents earning between $30k and$80k per year and maybe they should rezone some of the Oakridge area for rentals.

In September 2017 the benchmark price for an apartment property across the region was $635,800. This was a 21.7% increase from September 2016. In September 2017 the benchmark price for a condo apartment in North Vancouver was $553,500 up 19.5% in one year, up 54.4% in 5 years and up 60.0%i n 10 years. In Richmond the benchmark price was $598,600 up 26.4% in one year, up 73.5% in 5 years and 79.7% in 10 years. In Vancouver East the benchmark price was $535,600 up 23.4% in one year, up 75.3% in 5 years and up 90.6% in 10 years. In Vancouver West the benchmark price was $796,100 up 15.8% in one year, up 70.4% in 5 years and up 77.6% in 10 years. In West Vancouver the benchmark price was $1,153.700 up 15.2% in one year, up 66.5% in 5 years and up 60.0% in 10 years.

Westbank Corp, a prestigious developer with philanthropic goals, is under fire for maximizing their return on Joyce, a luxurious Eastside development that could have been built to reflect the working class neighbourhood around it and been affordable for local buyers. The City did not even try to fit an enormous project to their goal of affordable middle class housing by adding zoning requirements for social and market housing.

Again Westbank is in the news. The newest idea from Mayor Robertson’s platform is to offer pre-sales in Vancouver to local buyers for 30 days before they can be sold to outsiders. He held up the Westbank model in Horseshoe Bay West Vancouver as the template. According to people connected with that project they are discovering that people who signed agreements that are unenforceable are selling their pre-sale contracts and not planning to reside in the community. Even with the restrictions it appears that the price has risen from the original $875 per square foot to $1875 per square foot and nothing is built yet. Local politicians are bemoaning the fact that they did not require a percentage of rentals or market housing units within the project.

An enormous impact on the housing market will be the new tougher rules for mortgage lending that were announced on October 18 to begin on January 1, 2018.

As prices have risen the income required to afford a mortgage has risen too. Under CMHC rules any mortgage that did not have a 20%down payment required mortgage insurance. This insurance has been confused bythe public as being in their best interest. It is not life insurance on the mortgage it is financial insurance for the bank against loss. The outcome has been that the mortgage loans are government backed securities. CMHC started to worry that the Canadian government would be on the hook for $100 billion in guaranteed loans if borrowers cannot continue to pay their debts. In response the government requires all insured borrowers to qualify at a higher posted rate. This stress test usually uses the five year combined posted rate of the five large banks. It usually means a borrower has to qualify for two percentage points higher than the mortgage for which they are approved.

CMHC suddenly became aware that mortgages that were not insured because they had a 20% down payment were a debit against the financial system as a whole.They made up a huge portion of bank assets. As they worried they designed a program to address this problem. The Office of the Superintendent of Financial Institutions requires all borrowers to now qualify at the Bank of Canada 5 year posted rate. According to the Financial Post a borrower with 20% down can get a 2.97% mortgage today but will require 20% more income to qualify for the same mortgage under the new stress test rules. Independent analysts have added that the higher income requirement may be mitigated by a longer amortization period. The OSFI did not specify a certain length of time although they did comment that amortization periods still had to be within the allowable mortgage rules.

The concern of many is that borrowers will turn to the alternative financial markets not regulated by OSFI as the banks are. These mortgage specialists could become a much larger portion of the market. OSFI is only interested in the financial health of the banks in relation to the high level of consumer debt according to Superintendent Jeremy Rudin.

The real estate industry as a whole is concerned that the higher sales prices are limiting the number of buyers and that the stress test for mortgages will limit them further. This means that fewer younger Canadians will be able to afford to buy a home.

Garry Marr of the Financial Post reported that CMHC when discussing the influences on their portfolio as they performed stress tests to see how it would stand up had a list of potential problems. The new addition to the list was anti-globalization. They were looking at the rise of populism and the damage to economies by increased trade barriers. They looked at other influences but they did not combine the influences. They considered earthquakes, a steep decline in oil prices as well as an American style housing market meltdown as occurred in 2009 in the US.

Combined with China's limitations on their citizens taking money out of their country to invest in property overseas it may well be that this perfect storm does in fact impact prices in the Vancouver marketplace. We seem to be between a rock and a hard place.

High home prices, lack of inventory, crazy single-family zoning restrictions add to the mix. We shall see how it all comes out if the different levels of government finally get their acts together. Will let you know along with news of the Second Coming.

DT00KV

Nothing new. Actually, I’d be surprised if the prices went down.