There’s an old Scottish saying that ‘you should cut your cloth according to your stipend’ meaning to live within your means. It appears that local buyers are taking that idea to heart and making housing decisions based in reality, not dreams.

The Vancouver housing market is still going strong, not gangbusters like it did a year ago when offshore money was pouring into the detached housing market, but extremely active all the same. The detached market is recovering its mojo but the real demand is for townhomes and condos. Properties at each price point in all areas are receiving multiple offers and selling over the asking price.

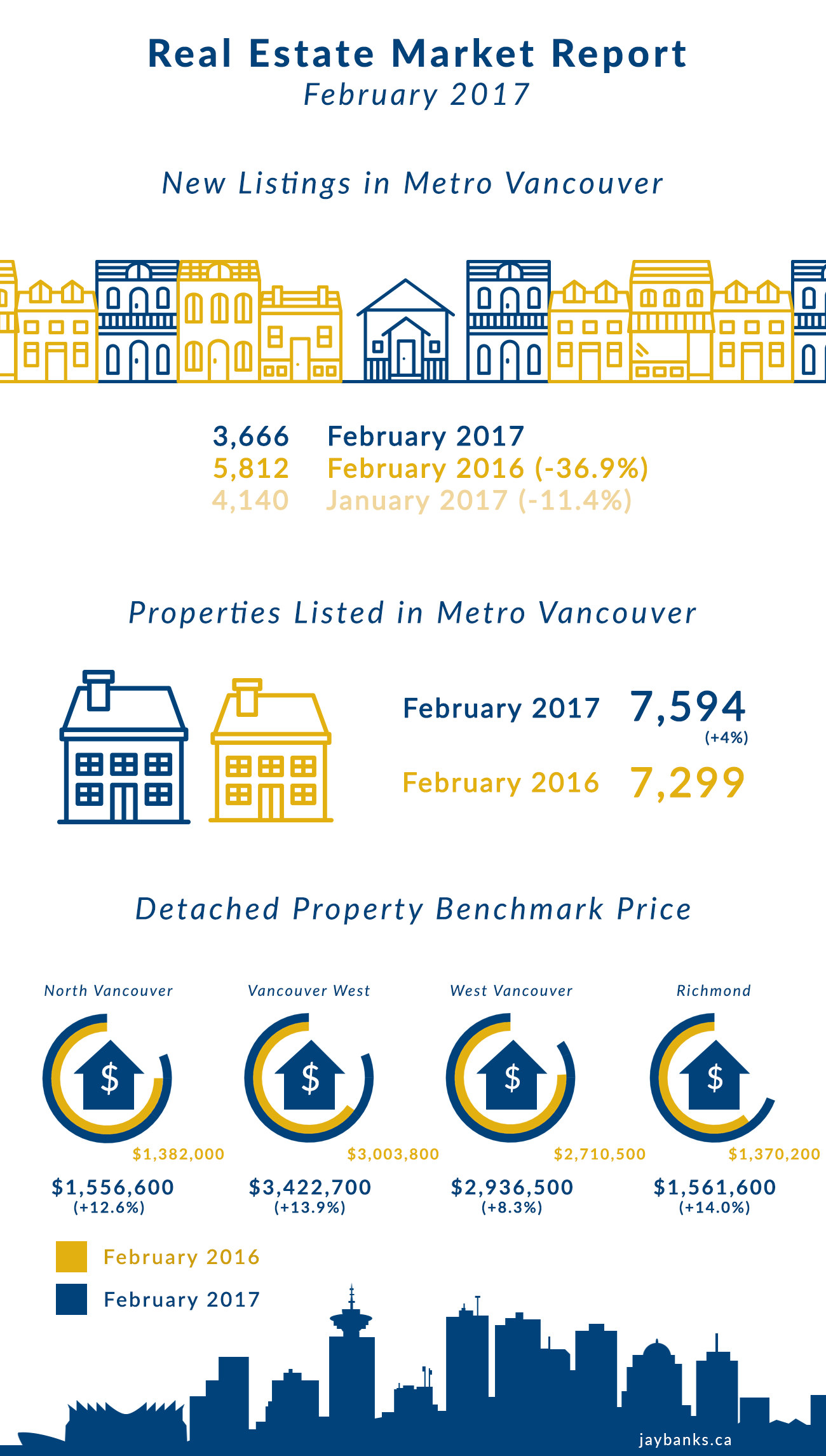

Condo properties in the city, close to transit, restaurants, and other amenities sell at a higher price point than further out. Buyers go where they can get a mortgage so North Vancouver near the Seabus is next on the desirability list. Richmond, where units are a little larger and less expensive per square foot but close to shopping, transit, and community centres, is attracting buyers. It’s 25 minutes from Brighouse across from the Richmond Centre to Waterfront Station with no downtown parking costs when you arrive.

With this change of attitude of buyers and with sellers worried that there is nowhere to go if they do sell the inventory is at a 14 year low for February. We are back to a Seller's market with the sales-to-active-listings ratio at 31.9% for February 2017, a 10 point increase from January 2017. A buyer’s market with lowered home prices occurs when the ratio goes below 12% for a sustained period of time, while a seller's market which we have enjoyed for the past several years occurs when the ratio is above 20% for that time frame.

No matter how it’s looked at affordability is a huge issue in Metro Vancouver. The MLS composite benchmark price for all residential properties in Metro Vancouver is $906,700 in February. This price is down 2.8% from the high of June 2016 and up 1.2% from January 2017. There is international financial institutional concern that the high price of homes and the amount of debt that borrowers are carrying is a danger to the Canadian economy.

In an effort to bridge the affordability gap the provincial government instituted a program called BC Home Owner Mortgage and Equity (HOME) to help qualified younger buyers with the difference between what they have and what they need as a downpayment to purchase. They can borrow up to $37,500 interest and payment free for 5 years. As always the devil is in the details. The loan has to be factored into the debt service ratio of 35% of household income required to qualify for the mortgage by the bank and the new federal mortgage rules require the borrower to qualify at the posted 5-year bank rate. This limits the number of buyers who can get a mortgage even with a minimum downpayment. It does assist younger first time buyers with a good paying job and closes to what’s needed for the downpayment. There is anecdotal evidence that this program is contributing to the number of multiple offers and sales over the list price on condominiums in the lower to medium price ranges. Everything that comes on the market sells if the building can be approved for CMHC financing. In some cases, the location or condition requires a higher downpayment but overall it is open season for condo homes.

There is a demand for investment apartment buildings as the rising prices in all home categories preclude purchasing by a large segment of the population. Rents are rising as fast as possible under the Residential Tenancies Act and any available loophole is being utilized. This includes fixed rate one year leases that can be increased without restriction at renewal. There is a rising concern in older buildings that new owners can evict long-term tenants in order to repair the units. The tenant can have first chance to move back in but most cannot afford the new rent. There is pressure on the municipalities to rezone for dense high rise rental buildings but many older walkup buildings will be razed in the process with old people, young people, new immigrants, disabled people with low incomes being unable to afford their neighbourhoods. The new town centres being developed along the Burnaby Skytrain line are replacing old with new in order to house the increasing numbers of people moving to the Lower Mainland.

In Metro Vancouver, a large portion of the rental housing stock is condominium investment properties. Unless the investor is a first owner and grandfathered as a landlord the strata council can hold a properly constituted meeting and the owners can vote to restrict the number of rentals. This also lowers the inventory. Almost any condo that comes up for sale is purchased by a user not investor. A recent Federal Court decision allows licensed medical marijuana users to grow their own drug inside their rental unit despite restrictions from the landlord and any ensuing damage. It creates fire danger for all the building residents but is now the law. A tenant can grow up to 60 plants, the landlord can lose his insurance and cannot evict the tenant. Sellers have to declare the past or present marijuana grow-op in their property when listing it for sale.

The Provincial Government is addressing the unintended consequences of the Foreign Buyer Tax on the recruitment of employees in IT and other specialized industries. With changes in the US business visa system, there may be more opportunities in Canada and local companies are trying to convince international talent to come to Vancouver. Everyone loves the city but not the housing prices, especially if a 15% surcharge is added to the existing property transfer tax. A work permit and paying Canadian taxes will exempt the non-Permanent Resident/Canadian citizen from paying the Foreign Buyer Tax.

There is a class action lawsuit from a group of Chinese buyers who are suing not to pay the Foreign Buyer Tax even though they are not Permanent Residents. They contend that the tax is discriminatory and that BC historically discriminated against people of Asian origin. Interestingly, as of November 2016, Hong Kong charges everyone buying a property a 15% Stamp Duty on the sale price. Only exceptions are Hong Kong Permanent Residents buying their first property. The HK property market was overwhelmed by Mainland Chinese buyers scooping up multiple homes at a time. Not that any level of tax is a deterrent to the most wealthy buyers in Hong Kong. A corporate buyer just paid HK$1.08 billion for a 9,950 s.f. house on The Peak and owes HK$324 million on the 30% Stamp Tax levy which includes the 15% "buyer’s levy" from 2012.

Douglas Todd of the Vancouver Sun writes that Canada Immigration has reported a large increase in Permanent Residents renouncing their status after 5 years. More than 21,000 immigrants over the past two years, mainly from China, India and South Korea, who qualified for Canadian citizenship refused it. They don’t want to meet Canadian requirements or pay Canadian taxes or declare income. They choose the 10-year visa program introduced by the Harper government. Under this visa, they can come and go on their passport of origin with no questions about working in Asia or spending sufficient time in Canada. Usually, children and spouses are living in Canada with the children going to school here until they graduate. Many return to Asia to work.

Todd in the Vancouver Sun also wrote on innovative tax schemes to cool the real estate market and create affordability. Some are practiced elsewhere to good effect. The idea is to level the playing field. People who don’t pay Canadian taxes and use loopholes in the tax system to evade CRA are speculating in Vancouver, Victoria and Toronto real estate. One option put forward by Ryan Kesselman, SFU policy specialist, advocates for a progressive property tax. Homes valued below a certain amount would be exempt. Percentages would increase to a maximum on houses over the limit. He suggested 0% below $1 million and 2% over $3 million. Those who pay Canadian income tax can offset the property tax. This way non-resident owners; those who own properties out of line with their income tax payments; speculators in residential properties; tax evaders; aggressive tax avoiders; criminals; astronaut families; nominee purchasers would all be paying an increased share of the tax burden. This system has been under discussion in Toronto where they are suffering the Vancouver syndrome of many foreign buyers and escalating prices.

Todd discussed the London purchase tax that has cooled the market there lately. The Stamp Tax is charged on a sliding scale from zero percent to 10 to 15% on more expensive properties. David Ley of UBC who wrote the book "Millionaire Migrants" proposes to tax the class of buyer, not the ethnicity. It’s clear that offshore investors will be returning to the Vancouver market and it would be a huge advantage to the provincial government to be pro-active on this issue. They can expand the effects of the Foreign Buyer Tax to actually help restore affordability to the third least affordable city in the English speaking world according to Demographia.

More anon.

JB00KV