A new day has dawned. Just not the one that all the pessimists were expecting. Properties have come off their mid-2016 highs; numbers of sales have declined from the end of 2015. Given that sales were already slowing by June 2016 it is a continuation of that progression of the market. A one year price increase of 35% mid-year for detached homes has fallen off to about 20% (except in West Vancouver where the one year increase ended at around13%) so no huge loss there.

There is currently a battle raging between home owners and the BC Assessment Authority over the 2017 tax assessments. The BCAA uses sales figures at July 1 of the previous year to set the valuations for the next year.This means that the 2017 assessments are set at the highest point in the market before the Foreign Buyer Tax crashed the party. The province had to raise the limit for the Homeowners Grant to $1.6 million in order to partly pacify their voters. The BCAA is about to be inundated with individual appeals of the assessments which have gone up 35-55% in one year. This means that municipal property taxes have gone through the roof.

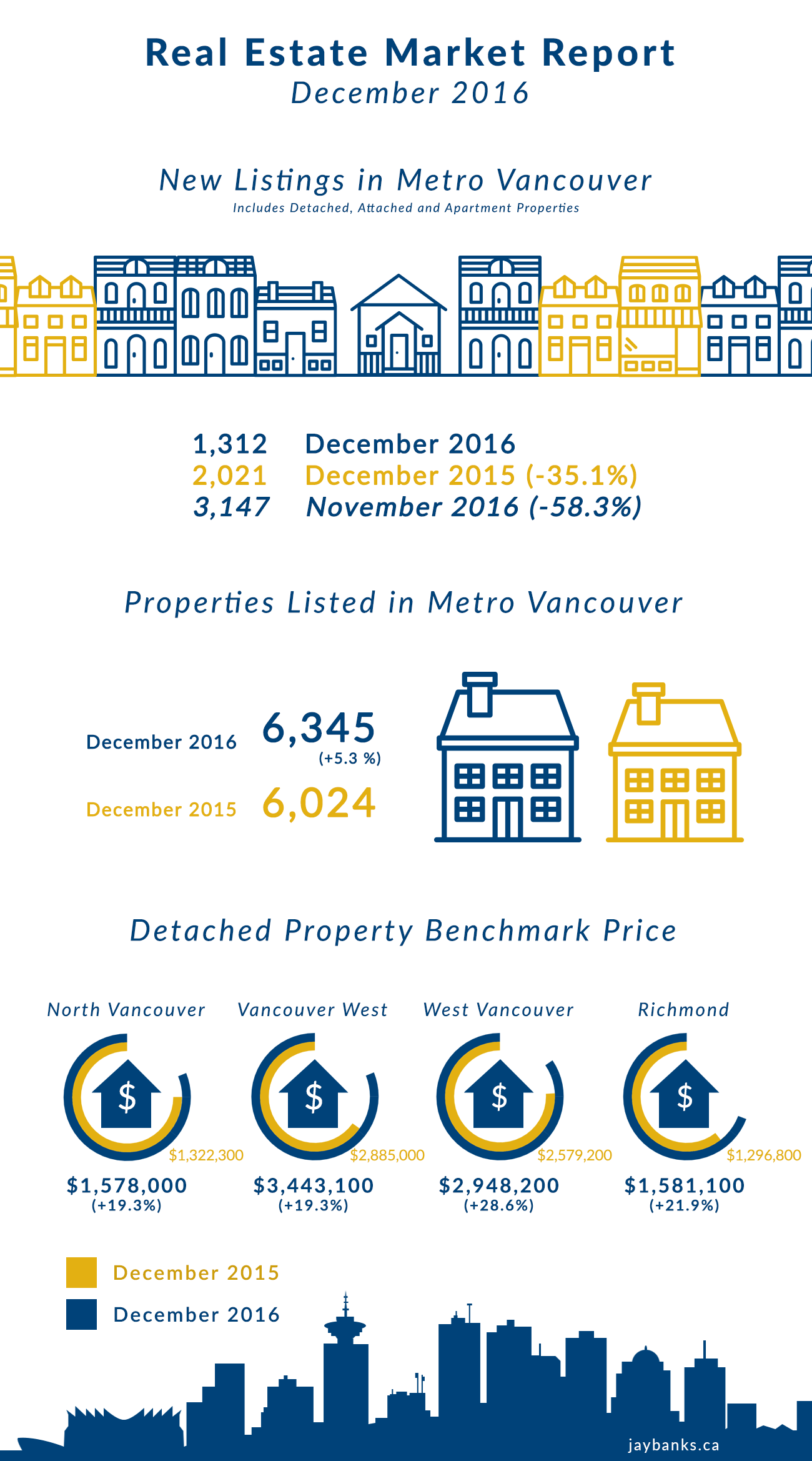

The Metro Vancouver housing market of 2016 was the third highest selling year after 2015 and 2005.

The MLS Home Price Index (HPI) composite benchmark price for all residential (detached,attached and condo) properties in Metro Vancouver finished 2016 at $897,000.This is a 2.2% drop over the past 6 months and a 17.8% increase over December 2015.

However, it is an active orderly marketplace. The big difference is the change of focus from detached homes to townhomes and condos. With all the offshore buyers looking for investments in high end properties there was a strong draw to that product. It wasn’t until unethical and illegal real estate practices by some companies/realtors/developers/investors were exposed by the Globe and Mail investigative journalists that the provincial and federal governments were forced by public opinion to close loopholes that had made Canadian, particularly Vancouver, real estate attractive to money laundering and abusive investment strategies. The province stopped the process that allowed contracts to be sold before completion and then resold at a higher price with no tax paid, commonly called shadow flipping. CRA finally had to deal with the laissez-faire approach they took to dealing with unpaid taxes and illegal claims of permanent residency with no capital gains tax being paid on the sale of empty homes.

These mechanisms to slow the high end of the market were topped off by the Foreign Buyer Tax imposed in late July that added a 15% surcharge to the existing Property Transfer Tax to be paid by non-resident buyers. The FBT has moved foreign investor funds from the Vancouver to the Toronto market that is now in the same position that Vancouver was in 2015/16.

Although homes are still selling with the Seller absorbing the Foreign Buyer Tax in the sale price the interest in detached homes has waned. There are newly built mansions in the $3 million range languishing on the Richmond market. According to the Vancouver Sun in BC only 8 properties over $3 million were sold to foreign buyers in November 2016 while 304 properties under $1 million were sold to foreign buyers.

Overall it appears that foreign buyers are also looking for cheaper real estate. This may become more apparent with the upcoming Lunar New Year celebrations when a billion Chinese go on the move throughout China and around the world to observe the New Year with family and friends. Those who come to Vancouver often use the visit to choose a home here.

With local buyers at the fore a different product mix is selling. Mainly due to high prices and the changing mortgage requirements by CMHC.

In Richmond and Burnaby where there is still a preponderance of Chinese buyers attractive livable homes under $1.5 million are selling well. Prices are down about 10-15% from their high. In Vancouver on the Westside, the most expensive location in Canada large properties are not selling at the pace they once did. With a benchmark sale price of $3.4 million the change is demonstrated in the number of sales in December 2015 (133) and 2016 (64).

Local buyers who have to pass the bank’s mortgage stress test to be qualified are being forced to consider townhomes and condos. This has put pressure resulting in multiple offers on well-priced properties. Yaletown in Vancouver with its high walkability score is particularly popular. Recently a mid-sized condo in an 8 year old building listed for $718,000 received 6 offers and sold for $780,000. Over 100 buyers attended the Open House.

According to the Vancouver Sun most surveys have shown that BC, especially Metro Vancouver, is the Canadian capital of loans from the Bank of Mom and Dad at 42% of first-time buyers receiving help from family. It would be impossible for most first-time buyers to put together a downpayment for the mortgage if not for this help. There has also been an uptick in bundled mortgages where buyers go to an unregulated mortgage company (MIC) for a secondary loan in order to qualify for the first mortgage. All legal but a sign of property prices being unaffordable without extra funds.

A danger on the horizon is the oppressive monetary policies of the Chinese government. Business news sources in the Vancouver Sun, Globe and Mail and elsewhere state that China has instituted new rules against transferring money out of the country to buy real estate around the world, particularly in Canada. Some see the new rules as inspired by the reports of Chinese investment in Vancouver real estate much of it funded from corrupt business and banking practices in China. The longer view is that China is trying to stabilize the yuan renminbi as a solid international currency in competition to the US dollar after allowing more overseas investment over the past two years. They now prefer to increase consumption and business expansion in China rather than see their citizens invest in other countries.

According to China-watching sources the government is concerned about its diminishing foreign reserves so no Chinese citizen can now convert their yuan renminbi into US dollars by transferring funds online. They have to go into the bank, sign a document requesting the funds, state why they want to move money out of the country. Apparently the requests are mainly refused. One person posted an application online with the reason stating he wanted to breathe again and live longer so was going to Canada.

The rule in place was that US$50,000 was allowed to be sent abroad by each Chinese citizen each year. Many family members would pool the money when it got to its destination. Now in addition to the increased disclosure requirements those exporting currency have to sign a pledge that it won’t be used to purchase real estate or securities.

The general consensus is that big corporations and investors who have substantial sums in foreign banks are not affected by this but the middle class buyers who have been purchasing most of the real estate in Metro Vancouver are affected. What impact this will have on the local markets is still an open question.

It may be that the optimistic forecast for a stable real estate market in 2017 was a bit premature. More anon.

JB00DT